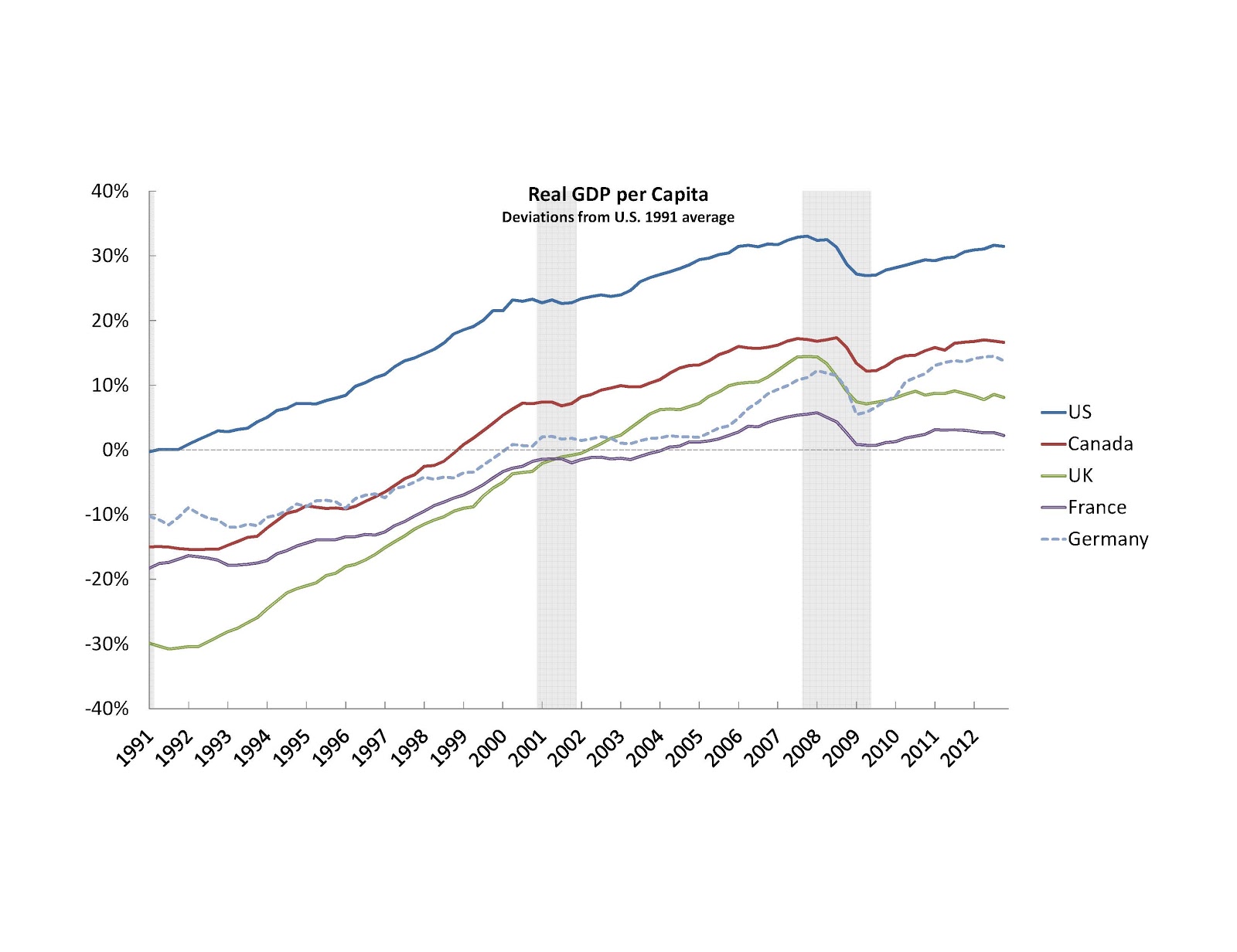

My colleague, Fernando Martin, has an interesting chart that plots the real per capita GDP of five industrialized countries since 1991:

The data above are expressed as percentage deviations from the U.S. level in 1991, with the initial position calculated using PPP converted GDP per capita from the Penn World Tables. Thus, in 1991, the U.K. is estimated to have had a real per capita income that was 30% lower than the U.S. Germany's real per capita income was only 10% lower than the U.S. in 1991, and so on.

The data above are expressed as percentage deviations from the U.S. level in 1991, with the initial position calculated using PPP converted GDP per capita from the Penn World Tables. Thus, in 1991, the U.K. is estimated to have had a real per capita income that was 30% lower than the U.S. Germany's real per capita income was only 10% lower than the U.S. in 1991, and so on.

Each of these countries experienced a similar decline in output during the most recent recession. But only Germany has the recession been "temporary." That is, only in Germany has real per capita income returned to its pre-recession trend. The other four countries exhibit persistent "output gaps"--their real per capita income remains below their respective pre-recession trends. Ah, Germany. All hail that Teutonic economic juggernaut.

But just hold on a second. While it is true that Germany appears to have weathered the economic storm better than others, it seems to have done so at considerable cost.

From 1991-2007, German real per capita income grew at a paltry 1.3% per annum. Compare this to the U.S. (2.1%), Canada (2.2%), France (1.6%), and the U.K. (2.9%). These are huge differences in long-run growth rates. In particular, while German income was only 10% below that of the U.S. in 1991, it is presently about 18% below U.S. income. That's called falling behind (albeit, at a steady pace).

And yes, the U.K. presently looks ugly. But it looks considerably less ugly when we take into account the growth record. In 1991, real per capita income in the U.K. was 20% below that of Germany. Just prior to the recession, the U.K. had just about closed that gap. Of course, things have not looked good for the U.K. snce then.

Fernando and I are also led to speculate on the role played by monetary policy for shaping the economic recoveries of these nations. France and Germany, as members of the EMU, operated under the same monetary policy--and yet, their recovery dynamics look very different. Also, since inflation was pretty low over this sample period, real and nominal GDP look practically the same. So for the NGDP targeters out there: it appears that German NGDP is back on target, but not French NGDP. Care to comment?

Moreover, out of this set of countries, only the U.K. has experienced a significant rise in inflation (and hence, NGDP). It's not exactly clear from this data how this "looser" monetary policy has contributed to a more rapid recovery dynamic (although, as usual, we have to be careful because many other things are happening, especially on the fiscal front).

Each of these countries experienced a similar decline in output during the most recent recession. But only Germany has the recession been "temporary." That is, only in Germany has real per capita income returned to its pre-recession trend. The other four countries exhibit persistent "output gaps"--their real per capita income remains below their respective pre-recession trends. Ah, Germany. All hail that Teutonic economic juggernaut.

But just hold on a second. While it is true that Germany appears to have weathered the economic storm better than others, it seems to have done so at considerable cost.

From 1991-2007, German real per capita income grew at a paltry 1.3% per annum. Compare this to the U.S. (2.1%), Canada (2.2%), France (1.6%), and the U.K. (2.9%). These are huge differences in long-run growth rates. In particular, while German income was only 10% below that of the U.S. in 1991, it is presently about 18% below U.S. income. That's called falling behind (albeit, at a steady pace).

And yes, the U.K. presently looks ugly. But it looks considerably less ugly when we take into account the growth record. In 1991, real per capita income in the U.K. was 20% below that of Germany. Just prior to the recession, the U.K. had just about closed that gap. Of course, things have not looked good for the U.K. snce then.

Fernando and I are also led to speculate on the role played by monetary policy for shaping the economic recoveries of these nations. France and Germany, as members of the EMU, operated under the same monetary policy--and yet, their recovery dynamics look very different. Also, since inflation was pretty low over this sample period, real and nominal GDP look practically the same. So for the NGDP targeters out there: it appears that German NGDP is back on target, but not French NGDP. Care to comment?

Moreover, out of this set of countries, only the U.K. has experienced a significant rise in inflation (and hence, NGDP). It's not exactly clear from this data how this "looser" monetary policy has contributed to a more rapid recovery dynamic (although, as usual, we have to be careful because many other things are happening, especially on the fiscal front).

David,

ReplyDelete"So for the NGDP targeters out there: it appears that German NGDP is back on target, but not French NGDP."

I wouldn't necessarily call myself an "NGDP targeter", but I'll still have a go...

No matter what your nominal target, to the extent that two regions don't constitute an optimal currency area, I don't see any reason why you would expect to be able to hit your target in both regions. If the natural rate is lower in France than in Germany, then a compromise policy will necessarily be too tight for France and too loose for Germany. If frictions in goods, capital and labor markets are low, then arbitrage might equalize those natural rates. But then, some capital (land) doesn't move under most circumstances, so even then returns may not be equalized across regions. I don't see how changing the nominal target can help us here.

K, here's a question for you. Do you think that the UK's growth record in the sample period above would have been very much different had the UK been part of the EMU? And if so, please explain why.

DeleteDavid,

ReplyDeleteYour question about the recovery of the Euro periphery vs. core and its relation to monetary policy has been discussed quite a bit in the blogosphere. The short answer is that the ECB's monetary policy has been effectively geared toward Germany's economy. Thus, at the advent of the Euro, the ECB policy rate was close to what a Taylor rule would predict for Germany, but far too low for the periphery. Likewise,since the crisis it has been close to what a Taylor rule would predict for Germany, but too high for the periphery. In both cases, ECB policy has been destabilizing to the periphery.

In retrospect, what has happened in the Eurozone should not be surprising. Applying a one-size-fits-all monetary policy to an area that does not fit the criteria of an optimium currency area is bound to create such problems. This was especially so in the Eurozone, since the ECB inherited the conservative, inflation-fighting culture of the Bundesbank and applied it to a motley crew of European economies.

Here are some posts I have done over the past few years on this point:

Post 1

Post 2

Post 3

David,

DeleteAs you know, I spent a considerable effort trying to understand the theoretical rationale for NGDP targeting. The argument appears to me to be very weak (that is, in relation to the arguments that support a simple PLT as an optimal policy, which I understand).

Your posts above do nothing to help me out in this regard. The basic argument seems to be that the EMU is not an optimal currency area, and that the ECB tailored its policy to Germany.

Maybe. But there seems to be a simpler explanation. Just take a look at the German (and for that matter, Japanese) growth record. Slow. Very slow. (Do you interpret this as the outcome of ECB policy? Just curious.)

I imagine that you might see the same pattern across different regions in the US (which I presume you would argue is an optimal currency area?), but I'd have to check.

I am just sceptical that any of this has very much to do with monetary policy. Take at look at the UK. They are not constrained by "German" monetary policy and yet...

I do not find your arguments persuasive. (But, as ever, I will try to keep an open mind!)

David, my reply was not an argument for NGDP but rather an argument for the importance of monetary policy. And yes, it was that EMU is not an OCA and monetary policy is tailored to Germany.

DeleteI am not sure why you are now looking at Germany's slow trend growth. Yes, it is slow but your original question was why did Germany have a mild recession relative to the other Euro economies. That is a different question and the easiest answer is the non-OCA nature of the Euro area and the German bias at the ECB.

Unlike you, I see monetary policy playing a huge role in the crisis. Like the Fed, the ECB failed to fully respond to the rise in broad money demand and that turned what should have been an ordinary recession into the mess we have today. Yes, there are deeper structural problems in Europe and the Eurozone is not an OCA. But this has been true for the past decade, so why did the crisis happen now? A failure of monetary policy.

David,

Deletemy reply was not an argument for NGDP but rather an argument for the importance of monetary policy.

Alright, but I was asking about NGDP targeting.

I am not sure why you are now looking at Germany's slow trend growth. Yes, it is slow but your original question was why did Germany have a mild recession relative to the other Euro economies. That is a different question and the easiest answer is the non-OCA nature of the Euro area and the German bias at the ECB.

That may be the easiest answer for you, but that does not make it correct. An even easier (and possibly correct) answer is "the faster you grow, the harder you fall." What's wrong with this answer?

Unlike you, I do not necessarily view cyclical phenomena as being independent of growth phenomena.

I wonder: would "Germany: The Price of Unification?" be a more accurate headline?

ReplyDeleteYes, it may very well be.

DeleteAnother reason might be that capital flows back from periphery to Germany.

ReplyDeleteAnother way to look at it: The euro caused sovereign spreads to converge. This created a windfall for the periphery, and that sparked a feedback loop in credit and property.

ReplyDeleteSince '08, sovereign spreads have merely returned to pre-Euro levels. This did not much affect Germany, although it did require an indirect bail out of the German banks (which, as ever, are blood hounds for credit crises).

When NGDP targeters complain the ECB is targeting German NGDP, what they are really saying is, "please re-converge sovereign spreads". Despite Draghi's attempts at fiscal policy, this is not something the ECB can accomplish.

An interesting take on matters, Diego.

DeleteDavid,

ReplyDeleteAny analysis of German performance since 1990 cannot ignore the important economic an political event that was German reunification.

http://en.wikipedia.org/wiki/German_reunification

The merger of the former FRG/West Germany with the communist DRG/East germany was a massive structural change for the German economy, including a 25% increase in population and the absorption of an obsolete phsyical and human capital stock.

To take an example, the unemployment rate was around 5.5% before reunification, and averaged 10% in the whole decade after reunification. Later on in the mid 2000s, the structural reforms carried by the Schroeder government led to the stellar performance of the Germany economy (both in terms of output and employment), which you can also see in your graph.

Juan,

DeleteI agree with you that unification was a big deal. Nevertheless, I do not think what I say above is inconsistent with anything you say. For the purpose of my argument, I don't really care what caused Germany's slow growth. The point is simply that Germany grew slowly (the brief period you highlight notwithstanding); and that rebounding back to this slow growth trend is not so amazing.

David,

ReplyDelete[Sorry about answering down here, I can't "reply" in my browser]

I think it would have been worse. If the UK had been in the euro zone Gilt yields would be *much* higher, more like Spain's or Italy's, because of default risk. The direct impact of funding costs on government spending is clearly contractionary. This looks to me like a dead weight loss of the euro zone compared to sovereign currency issuers.

So while short rate policy was actually pretty similar in both jurisdictions, lower bond yields in the UK led to inflation, devaluation and reduced pressure on spending which was surely helpful. So I'd agree with you that the difference is not so much monetary policy as monetary *framework*.

Oops! You said EMU, not Eurozone. Denmark, not Spain. Then, no, I think things would have turned out pretty well the same. Maybe a bit worse without the benefit of devaluation, but no big difference.

ReplyDeleteThat's what I would figure too.

DeleteThat said, I do think that there is a sense in which the UK slowdown was a result of excessively tight monetary policy. Ie the real rate was too high. Unlike the Internet Monetarists I just don't think there was anything the monetary authority could do about it, being up against the ZLB. In a cashless world with -5% interest rates, maybe we all could have avoided that huge dip in your graph.

ReplyDeleteDavid Beckworth is quite correct in his description of monetary policy under the ECB. But it is not simply a question of Germany being the most powerful player.

ReplyDeleteIn the run-up to the start of the Euro in 1999 there was concern that that France and other countries would be forced to raise short rates as the ECB imposed a Eurozone wide average. Trichet argued strongly that if the periphery countries could not have low inflation with interest rates set at the level which suited core, low-inflation countries they shouldn't be in the Euro. he got that right. But it was of course far to late to say that the periphery should be excluded. So rates were set in line with French and German rates, seen at the time as a gesture of confidence in low inflation. It was also handy because Germany was in trouble.

After a period in which the currency weakened a lot through capital flows, the need for low rates in the core ceased. But by then the habit of the ECB in Frankfurt setting the rates which suited the Bundesbank in Frankfurt was well established.

Yes, either that or: Germany is a slow grower, and reverting back to this slow growth trend is not a great achievement.

DeleteBut I guess you'd rather explain secular regional disparities in terms of a common monetary policy.

David,

ReplyDeleteAgain another post that is interesting, but at the same time, seems to need a warning label reading: Caution: Correlation does not equal causation and is often only bias hiding behind selected facts.

Seems to me that one could argue that the years in question tell us an entirely different story, one about profits flowing to finance. That might explain, or tend to explain, GB's performance.

Here is a debt to GDP chart.

http://www.usgovernmentspending.com/downchart_gs.php?year=1792_2012&view=9&expand=&units=p&log=linear&fy=fy12&chart=H0-fed&bar=0&stack=1&size=m&title=US%20National%20Debt%20As%20Percent%20Of%20GDP&state=US&color=c&local=s

Does anyone want to go back to 1980?